Overview

Come October, it is time for a Q and A on the two big Acts. We asked you for some of your burning questions about the implementation of IIJA and IRA. Thank you to those who sent through questions. We have conferred with experts at the Department of Energy and scoured available resources to bring you the latest. Still, many specifics remain unknown, and we expect more clarity to come with future program guidance.

We also know that there is a wealth of knowledge in this community. If you have insights on any of the questions below, we welcome your input. Please get in touch!

The Tax Credits

Funding For Cities

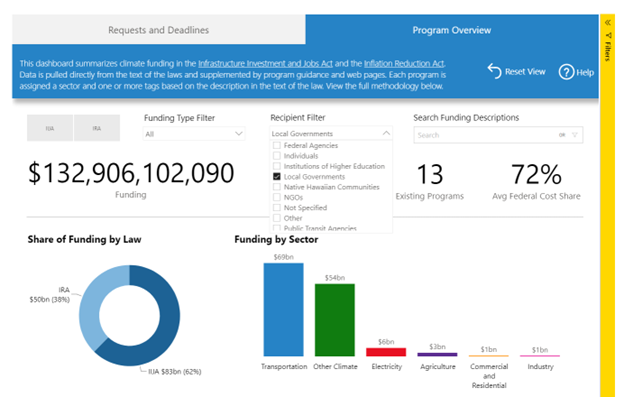

The first thing to note is that it is possible to filter by recipient on the Dashboard. See the image below. This may not solve the problem but can get you some of the way there.

Next, some of the most recent solar funding opportunities are here: Bipartisan Infrastructure Law Programs | Department of Energy. More specifically, we have seen the following:

- Funding Notice: Solar and Wind Grid Services and Reliability Demonstration | Department of Energy

- Pumped Storage Hydropower Wind and Solar Integration and System Reliability Initiative | Department of Energy

Here are some other programs that may be available to cities for solar projects:

- Greenhouse Gas Reduction Fund includes $7 billion for state, local, and tribal governments or nonprofits to deploy zero emission technologies.

- Environmental and Climate Justice Block Grants has $3 billion to implement community-led projects to remediate environmental risks to public health.

- Energy Efficiency and Conservation Block Grant Program has $550 million to assist local governments, states and territories, and Tribes implement strategies to reduce energy use.

- Clean Energy Demonstration Program on Current and Former Mine Land must fund at least two solar projects on former mine land.

- Renewable Energy Projects has funding for pilot geothermal, wind, and solar energy projects.

Justice 40

Portal Access